Connectivity

Introduction

The fourth industrial revolution has brought about a new generation of edge computing, connectivity and cloud applications that, in turn, require reciprocal investments in distributed technologies and infrastructure. The Internet of Things (IoT) — a decentralized system of interconnected communication networks and devices — is a convenient term used to encapsulate a development that delivers tangible benefits to individuals, businesses, society and the global economy.

Wireless connectivity and device management play a vital role in the IoT ecosystem. It is more than simply a transport medium but a dynamic and interoperable framework of communication protocols, SIM provisioning tools, asset management interfaces and cross-carrier associations. It enables enterprises to manage massive numbers of edge devices remotely, perform complex billing functions, codify KPIs and business rules and take advantage of powerful goal-seeking logic that optimizes cost, coverage or functionality.

Wireless connectivity and device management also impact industrial structures and boundaries by enabling organizations to offer customer-centric service delivery models, penetrate new markets and uncover lucrative monetization opportunities. It is changing the nature of competition by providing enhanced ecosystem visibility, tighter track and trace functionality and unfettered access to large volumes of relevant, timely edge data. Predictably, this is having a positively disruptive effect across the supply chain. It is raising a new set of strategic choices related to how edge data is generated, managed and monetized and how value is created, captured and sustained. Relationships with customers and stakeholders are also being redefined and their traditional roles are changing in line with the pervasive information revolution. Emblematic of what many are calling the knowledge economy, the IoT has now displaced cloud as the second most important digital transformation initiative among organizations, with mobile still ranking marginally higher in importance.

This paper seeks to highlight various trends in the IoT connectivity market and uncover criteria important to organizations in their IoT investment decisions.

Snapshot of the Global IoT Connectivity Market

Scale of the Connectivity Market

The global connectivity market is multifaceted, localized and competitive. It is comprised of a diverse collection of providers, networks and standards that, combined, address the increasingly regionalized data requirements of an equally diverse set of industries and use cases. Global connectivity providers are increasingly leveraging their commercial relationships, thereby aggregating their cellular and non-cellular networks into a single virtualized platform capable of cloud and network services.

Cellular networks continue to service most global data connectivity requirements across consumer and commercial markets, of which IoT subscribership, as of 2017, totaled 648 million or nearly 8% of the global market, an increase of 56% YoY.1 The number of IoT devices in use worldwide, as of Q2 2018, is reported at 7 billion.2 Although trailing by a factor of 12:1, the IoT connectivity market is poised for significant growth across all public and private sector segments with the number of IoT subscribers forecasted to total 2.7 billion by 2022 at a global compounded annual growth rate (CAGR) of 33.1%. Global revenues during this period are expected to increase from $7 billion to $23.5 billion, a CAGR of 27.3%.3 The cellular IoT connectivity market is positioned for significant, continued growth worldwide, followed by a steady expansion of low-power wide-area (LPWA) and satellite markets as new use cases demand and emerging economies mature.

In Q2 2017, Europe and the Americas lead in IoT cellular subscriptions globally, reporting 165 connections per 100 people, followed closely by emerging economies of China, Brazil, Russia, South Africa and Turkey. Russia and Brazil each reported 70 connections per 1,000 people. South Africa and Turkey reported 5.3 million and 4.2 million cellular IoT subscribers respectively, on par with South Korea and Japan. India and Pacific Rim countries with large populations offered sizable yet unrealized market potential.4

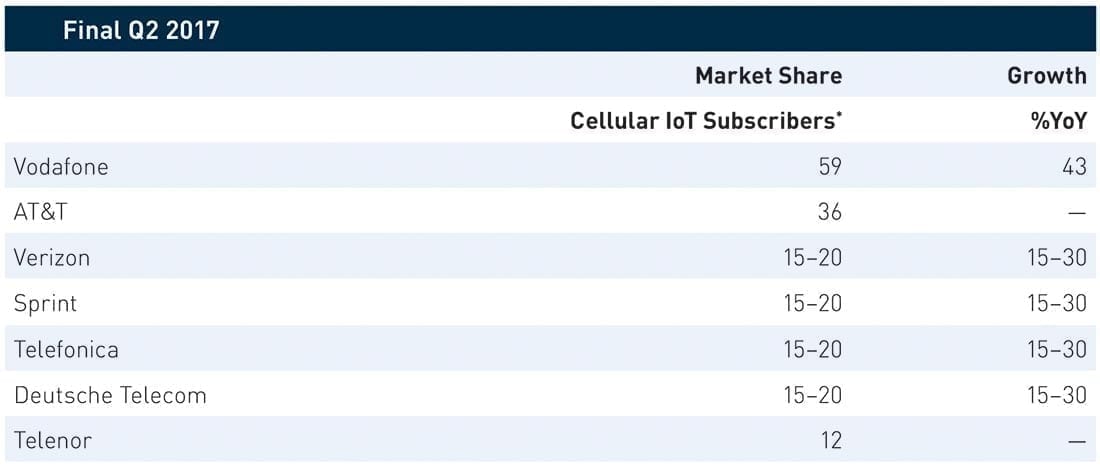

The unprecedented growth of the IoT connectivity market is actualized by the mass adoption of fourth industrial revolution technologies and methodologies that build on the widespread availability of distributed edge computing and big data cloud applications. The global IoT connectivity market is also going through massive changes driven by large technology and digital infrastructure investments. The number of cellular IoT connections is expected to reach 4.1 billion in 2024, of which 2.7 billion will originate in Northeast Asia. NB-IoT devices will grow at a CAGR of 41.8% from 106.9 million units in 2018 to 613.2 million units in 2023, largely driven by Northeast Asian markets. This is expected to have a profound and effect on 2G, 3G and 4G networks, driving the global price of IoT modules and chipsets below the $2 mark. Outside the APAC region, Vodafone reported 59 million subscribers at a growth rate of 43% followed by AT&T reporting a subscriber base of 36 million at the close of Q2 2017. Verizon, Sprint, Telefónica and Deutsche Telecom rounded out lower-tier providers, reporting in the range of 15-20 million subscribers, with Telenor at 12 million cellular IoT subscribers. Together, these mobile operators account for approximately 33% of the global IoT cellular connectivity market.5

IoT Connectivity Networks

Today, IoT connectivity includes a spectrum of heterogeneous communication technologies spanning cellular, LPWA and satellite networks. Although over 500 million devices were connected to some form of wide-area network as of 2017, no one network standard offers optimal cost, throughput and coverage across all use cases.6 Nor is any singular mobile network operator (MNO) capable of providing true, single-source coverage across all regions. The IoT connectivity market is diverse and divided into multiple ecosystems along technological, regulatory and political lines. Moreover, networks are constrained by immutable physical laws governing how quickly and far packets of information may be wirelessly transmitted from one to another. The high data throughput offered by 5G cellular may apply to autonomous vehicle (V2X) or media-intensive use cases, but its limited coverage area and high operating expense (OPEX) precludes its use in remote oil and gas or mining applications.

Cellular

The cellular network space is becoming more technologically diversified to meet the needs of increasingly complex data requirements. The 3GPP platform is the leading standard for cellular technologies, operating across multiple modes and frequency bands. The evolution of standard may be divided chronologically: Legacy 2G/GPRS, current 3G/4G HSPA/LTE and emerging 4G-MTC that includes LTE-M and NB-IoT. In the context of 5G, according to a recent GSMA whitepaper published last year, 3GPP has agreed to support evolving NB-IoT and LTE-M standards and address LPWA use cases within the broader 5G specification. Release (Rel) 14 NB-IoT and LTE-M will coexist in the same networks as other 5G New Radio (NR) components.7 These 5G NR components are designed to specifically address diverse deployment models, spectrum usage and new device capabilities. LTE-M and NB-IoT communications will also operate within 5G NR frequency bands. This move is significant as it enables IoT providers to future-proof capital investments in LPWA technologies. It also empowers IoT early adopters with an effective and expedient mechanism to transition to the latest 5G mobile broadband technologies via a predefined evolutionary pathway.

Originally designed for encrypted voice communication, 2G is a highly efficient standard that offers low-speed mobile data services and SMS functionality. As of 2016, 2G IoT connections worldwide were just shy of 300 million, accounting for a market share of 75%. The standard, however, is not optimized for data and will be finally decommissioned in many countries as of 2020.8

4G remains the leading network for connecting advanced mobile devices. By 2020, market share is projected to increase to over 70%.9 However, for all but the most media-intensive IoT use cases or topologies that include data-aggregation IoT gateways, the standard’s high-throughput low latency comes at the cost of increased radio complexity and power consumption. In 2014, the LTE CAT-1 was added to address the IoT use cases and low data-usage requirements. As of 2016, 3G and 4G only comprise an estimated 16% and 9% of IoT connections respectively. In the U.S., AT&T is actively reallocating capacity away from 3G to more advanced wireless networks and encouraging business customers to transition to its 4G LTE and LTE-M networks. Verizon is following suit by discontinuing CDMA 3G and 4G non-HD Voice services after 2019. Vodafone UK is planning to disconnect 3G services within the next two to three years and reallocate spectrum bands to its 5G network.

Efforts to retire 2G networks are less resolute or straightforward due to continued global reliance on 2G cellular for M2M communications and the need for low-cost network connectivity in rural parts of many countries. In the U.S., AT&T, Verizon and T-Mobile have all announced plans to shutter their legacy 2G services, yet sunset strategies between these three carriers differ markedly. While AT&T announced that it would shutter its 2G network on January 1, 2017, T-Mobile promptly announced it would “throw a lifeline” to AT&T IoT by offering free SIM cards.10 Meanwhile, Verizon plans to terminate CDMA1X 2G network by the end of this year while gearing up to offer Cat 1 as an alternative to 2G IoT.11 However, the carriers are in common agreement that spectrum allocations need to be reassessed and, in all likelihood, reprovisioned among emerging mobile broadband HSPA-based offerings.

4G-MTC (LTE-M/NB-IoT) is an emerging standard optimized for massive IoT deployments across a wide range of IoT use cases including support of reduced transmit power, bandwidth and overall power consumption. 3GPP Release 14 also introduces support for positioning (that complements or replaced GNSS) and single-cell multicasting providing the ability to broadcast messages and firmware updates to large numbers of IoT devices. The release also includes a new Cellular V2X (C-V2X) standard with support for communication between vehicles and infrastructure (V2I), pedestrians (V2P) and other vehicles (V2V).

Satellite and LPWA

LPWA operates in the unlicensed Industrial Scientific Media (ISM) bands and is designed for low-cost, medium-range communications in which power consumption and battery life are limited. Satellite data networks offer ubiquitous planetary coverage, providing connectivity in remote regions or for critically important applications, including maritime, transportation and public sector use cases. Mobile satellite services (MSS) include messaging, voice and data communications via short burst data (SBD) services. The low earth orbit (LEO) constellation of satellites currently provides the bulk of IoT connectivity, divided between the four mobile satellite services (MMS) operators: Orbcomm, Iridium, Inmarsat and Globalstar. However, incumbent providers are expected to face stiff competition from large start-up LEO satellite providers, including OneWeb, SpaceX and Amazon, with the latter confirming plans to launch a constellation of over 3,000 satellites code-named “Project Kulper” to provide high-speed broadband connectivity to over 95% of the world population. Iridium and OneWeb have recently entered a collaborative MoU to jointly develop complementary full-service options for applications including heads of state communications, critical tactical services, maritime and disaster response. Each company leverages different capabilities of their respective LEO constellations and bands (L-band and Ku-band). Paris-based global satellite operator, Eutelsat Communications, is developing Eutelsat LEO for Objects, an IoT constellation of CubeSats sourced from U.S. nanosatellite manufacturer, Tyvak International, in partnership with LPWA provider, Sigfox, the company planning to launch a total of 25 nanosatellites over the next three years.12

The global market for IoT nanosatellite services is forecasted to accelerate wildly between 2021 and 2022 and reach $5.9 billion by 2025.13 It is also expected the slower growing (albeit larger) LPWA market will not directly be affected by growth in the satellite market over this period. By 2024, satellites will be responsible for an estimated 24 million IoT connections with significant growth in agriculture, maritime asset tracking and aviation.14

Challenges and Pitfalls in Selecting an IoT Connectivity Partner

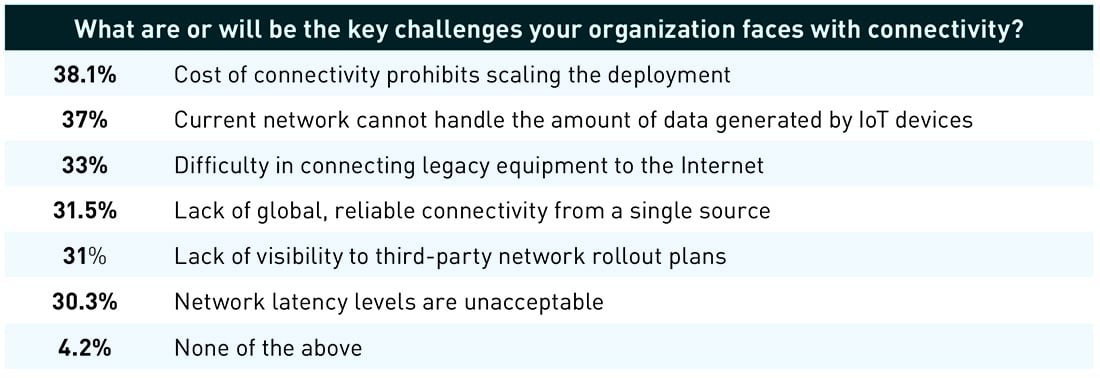

The IoT connectivity market is complex and comprised of tightly integrated hardware, software and cloud services. It is also highly subject to carrier network certification requirements and government regulations, both in terms of pre-deployment activities, including design, certification, licensing and post-deployment management, and support operations. This tight-knit IoT connectivity development and rollout approach underscores the importance of selecting a qualified IoT solutions provider. It reveals several perceived and real challenges faced by system integrators and enterprise customers alike concerning IoT connectivity service development, adoption and usage. In a 2019 survey of 4,480 organizations, respondents ranked cost and a lack of available bandwidth for data-intensive IoT applications as leading factors when asked to cite key connectivity challenges faced by their organizations. Other top concerns included ineffectual legacy hardware integration support and difficulty in retaining services from a reliable single-source connectivity provider.

This survey offers a quick snapshot of some of the leading connectivity concerns organizations are facing, yet it does not provide a complete picture of the wider connectivity challenges. A closer inquiry is needed to reveal the underlying factors negatively impacting cost, capacity, interoperability, usability and security, and how emerging technologies, alliances and solutions propose to address these challenges.

Commercial Carrier Relationships

Enterprise IoT ecosystems are not simply collections of fixed assets functioning in a microcosm but are living, breathing systems of connected people, mobile assets and intelligent devices. The increasingly remote, uninhabited and mobile nature of many IoT deployments requires a new approach to IoT connectivity, one that elegantly reconciles often conflicting criteria of cost, usability, functionality, security and access. Only IoT connectivity providers with multi-carrier offerings across cellular and a proven track record of delivering IoT connectivity platform services worldwide are competitively positioned for sustained profitability and growth. The ability to aggregate multiple networks on a shared core infrastructure is mandatory. From a technical standpoint, harmonizing multi-carrier networks offers intrinsic advantages of coverage, cost savings and flexibility, yet this capability is not as much a question of technical proficiency as it is of commercial competency. Competitive advantage lies in the strength of underlying commercial relationships between the connectivity provider and the carriers.

Demand for seamless international cellular IoT connectivity is on the rise, especially for multinational, centralized manufacturing operations with globally distributed supply chains and other cross-border IoT enterprise use cases. This demand necessitates a unified IoT connectivity platform that supports pre-negotiated SLA roaming services for low data volume and access to advanced connectivity options via multi-MNO service architectures for those with critical or high volume requirements, such as those in the telematics, fleet and V2X industries. This multi-domestic connectivity approach to international coverage unlocks access to multiple carriers SIMs via bilateral or multilateral alliances, depending on destination. Establishing unilateral agreements with these carriers instead of or in addition to a broader carrier alliance is therefore essential to ensuring comprehensive and reliable multi-domestic IoT connectivity service.

IoT Network Technologies

In 2017, cellular, satellite and LPWA networks were responsible for connecting over half a billion IoT devices. Today, that figure is estimated at 7 billion devices. Wide area networks are becoming highly diversified as next-generation connectivity technologies adapt to accommodate the needs of new use cases and emerging markets. The 3GPP family of low-power cellular standards continues to command the largest market for wireless IoT communications worldwide; however, small form factor (micro and nano) satellite technologies and LPWA unlicensed ISM bands are proving potentially viable, especially for remote or low-power applications.

The zealous pace of technological innovation among the family of 3GPP cellular standards is forcing IoT connectivity providers to remain relevant or risk losing significant market share. 3GPP Release 13 introduces a new category of standards to address M2M communications. The category includes the 2G EC-GSM standard and two 4G standards (i.e., eMTC/LTE-M and NB-IoT) that, in most cases, may be acquired via software updates. Of these standards, NB-IoT, an LPWA technology, is gaining worldwide support from leading carriers in Europe (i.e., Deutsch Telekom, Vodafone, Telefonica, etc.) and APAC (i.e., China Mobile, China Telecom and China Unicom). This support is partially due to the standard’s ultralow complexity, enhanced security safeguards and broad support by major mobile equipment, chipset and module manufacturers. NB-IoT delivers significant improvements in power consumption, system capacity and spectrum efficiency and is backward compatible with 2G, 3G and 4G networks.15

As the IoT platforms diversify and mature, connectivity providers are transitioning from reliance on carrier-bound SIMs to bearer-agnostic operating models. This move has important and far-reaching implications on the IoT device provisioning, management and data collection functions by addressing the logistical challenge of managing a massive number of devices, services and accounts across multiple carriers. The model also clarifies the roles and responsibilities for each service class and delineates the custody chain of IoT assets and data in the ecosystem. From a technical standpoint, actualizing a bearer-agnostic solution model is predicated on proficiency in implementing emerging embedded SIM (eSIM), embedded universal integrated circuit card (eUICC), international mobile subscriber identity (IMSI) and other virtualized SIM aggregation technologies. The eUICC virtual interface eliminates the need for onboard connectors and obviates the logistical complexity of preprovisioning large numbers of physical SIM modules. The interface also allows SIM configuration and activation to be deferred until the unit arrives at its destination. In effect, it nullifies the lock-in effect to one carrier, resulting in simplified distribution, subscriptions and carrier management. eUICC also facilitates greater interoperability between adopters, notably in industries with a high degree of hardware variability such as the connected vehicle space.

Purposeful Enablement

Many across various engineering circles are inclined to tout the technical accomplishments of global IoT connectivity innovation; however, the real value is achieved on a broader economic, societal and environmental scale. Commonly conceived as purely utilitarian or routine, all too often IoT connectivity is designed, implemented and managed on the underlying objective of boosting efficiency through automation or optimization routines. In the race to digitize, far less thought was given to the potential of its real value: providing the means (not the end) to solving real-world data connectivity challenges, predicated on exacting customer, industry or regional requirements. IoT connectivity providers offering proven technologies, expertise, and knowledge to unlock rapid prototype, development and actualization of industry-centric use cases — including V2X fleet telematics, cold chain, shipping and other mobile track-and-trace applications — are well-positioned for growth in these industries.16

Today, IoT connectivity providers have pivoted from a cookie-cutter approach to building holistic platforms of interoperable development, management and track-and-trace experiences that span the connectivity service delivery cycle from concept through end-of-life. This purposeful approach centers on addressing the needs of people and, by extension, their organizations and industry verticals. More people-centric IoT connectivity models are focused on enhancing the development, deployment and management of complex IoT ecosystems. People-IoT interaction UX, context-aware applications and big data analysis are some of the tools being looked at by leading IoT connectivity providers to stream and enhance D2D, M2M and P2M information flows.

OEMs are transitioning from chip-level design to third-party cellular modules that may be integrated into their IoT devices easily. This shift offloads the cost and complexity of designing, testing and certifying the core components of the IoT device to the IoT connectivity provider or hardware manufacturer. It also enables OEM to allocate resources to revenue-generating activities and strengthen core competencies. Enterprises may also benefit from multi-domestic certification programs offered by international M2M associations that pool development resources and provide access to several preapproved chipsets. The Global M2M Association (GMA) module certification program, launched in 2015, is an example of such a type of bilateral cooperation agreement. Other options include direct multi-carrier certification approval facilitated via IoT connectivity provider-negotiated terms and 2G upgrade roadmaps for an easy and cost-effective transition from GSM/GPRS and CDMA 2G to newer cellular standards. As of 2017, AT&T had over 24,000 developers actively using its IoT certification platform, with Verizon and Sprint offering comparable certification programs.17

IoT connectivity platforms continue their transition to granular, vertically siloed offerings in post-development. More mobile use cases are demanding highly sophisticated track-and-trace connectivity services capable of orchestrating complex asset deployments, provisioning large numbers of IoT SIM devices, delivering bulk OTA maintenance upgrades and effectively managing multiple carrier relationships. These include the transportation, distribution, logistics, utility, energy, heavy equipment and mining sectors with use cases ranging from dry goods and cold chain fleet asset management, rail and V2X automation. Planning, designing and managing complex IoT deployments of mobile edge devices, localized aggregation gateways, data networks and security protocols require a connectivity provider capable of delivering a corresponding degree of orchestration, coordination and organization complexity.

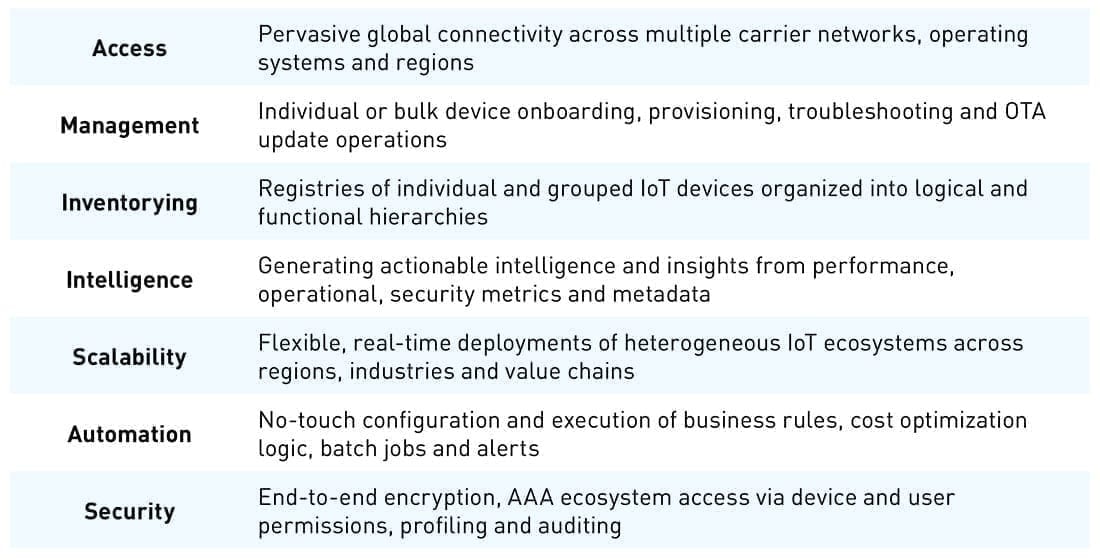

The following table highlights several value-added functional areas in use by leading IoT device and connectivity operators:

Enterprise IoT Connectivity Investment Trends

It is instructive to identify the latest investment trends within the sphere of current and planned enterprise IoT initiatives to present an accurate assessment of the IoT connectivity market. Of the leading digital initiatives, IoT has taken the second spot for the first time, behind cloud transformation. This section highlights the top purchasing criteria and expectations cited by enterprises across 29 countries and six industries that have at least 100 employees. These results offer insights into market drivers that underpin investment decisions by enterprises at the front line of the economy.

Investment Spending

Enterprise IoT investment worldwide is gaining traction. Sixty-one percent of organizations have already deployed their IoT initiatives, and 27% intend to do so within the next 12 months. APAC slightly leads the Americas in current IoT deployments. Of these, 85% of organizations have a budget allocated specifically for IoT projects, and 54% of this budget is under the control of IT departments. It is worth noting that IT departments control IoT budgets, despite a general misconception that line of business (LOB) units retain the purse strings. This point is interesting, as distributed IoT operational technology (OT) and centralized IT ecosystems stem from different corporate charters and exist in disparate data and functional domains. At the enterprise level, 36% of organizations prefer to acquire technology independently (of vendors) and contract with third-party integration to implement the solution.18

Success Rates and Measures

Enterprises are also nimbler and more responsive when it comes to IoT adoption with an average of 77% of IoT projects determined unsuccessful within the order of weeks or months. Companies capable of quickly determining when projected costs exceed value forecasts are better positioned to take premeditative steps to reassign resources to revenue-generating initiatives. This assumes that these enterprises have achieved a high degree of agility in planning and measuring via KPIs and circular-feedback mechanisms. While each industry has different KPIs when measuring success, overall, organizations prioritize operational efficiency, productivity gains, customer satisfaction, cost savings and safety improvements in ascending order of importance. It is instructive to consider how these priorities differ between sectors.19

Market Drivers

The top five factors driving IoT adoption in 2019 include improved internal business productivity; lower operational OPEX; improved product quality; improved security; and increased customer productivity. It is noteworthy that although economic factors rank high, less tangible metrics of quality, security, customer experience and better decision making are gaining importance. Of the driving forces compelling organizations to embark on IoT projects in 2019, 78% stem from internal requirements and teams, with the balance coming from external forces such as customers, partners, competitors and regulatory organizations.20

The leading challenges cited by IoT adopters in 2019 include deployment-related CAPEX and OPEX, security and lack of internal skills in the areas of technology, strategy and operations. These concerns dovetail nicely with IoT connectivity provider value propositions that focus on providing cost savings, chip-to-cloud security, development and support framework of engineering, sales/SMEs, certification/QAQC and professional implementation services. Not surprisingly, topping the list is security and data privacy, followed by performance, system interoperability, information processing and analytics.21

As previously discussed, IoT connectivity providers are moving away from generalized technology models in favor of highly interactive, compelling, people-centric solutions. 2019 saw significant growth in the implementation of people-centric solutions, followed by building, environment, video and vehicle projects.22

Conclusion

The digital connectivity market is maturing. Its transmutation has eclipsed the carrier-centric limits of its capability and potential. In the knowledge economy, information is the lifeblood of a healthy, sustainable global market and connectivity and the means to realize the meaningful exchange of information between people, systems and things. Under the digital transformation banner, hardware and software combine to deliver not only discreet services but also synergetic connectivity experiences that leverage multiple networks and technologies.

IoT edge devices, connectivity and data delivery mechanisms have also evolved (and diverged) from the traditional broadband model. IoT devices are far more mobile, edge-distributed and numerous than ever before. They also require enhanced security and intrusion protection at every level of the connectivity chain, from embedded sensors, processors and chipsets right up to the cloud. The nature of the mobile IoT connectivity topology also means that cellular handoffs between disparate carrier networks must be seamless for connection and service functionality.

This begs not only a new approach to IoT connectivity but also a partner with the global clout, commercial ties and technology experience to effectively obviate risk and unlock long-term value, profitability and growth. Companies including Cisco and Ericsson — who trace their lineages to centralized computing networks and telephonic hardware respectively — have managed to channel considerable resources into a diversified offering strategy that, today, helps them propel the global IoT connectivity management segment. However, several M2M pioneers, whose value propositions include telecommunication modules, connectivity management services and cloud analytics platforms, have emerged to disrupt the IoT market significantly.

Today, enterprise connectivity ecosystems are comprised of a kaleidoscope of interoperable technologies spanning maritime, terrestrial and near-earth-orbit domains. Regional constraints persist, yet the trend is for more open, interoperable and standardized connectivity services that transcend political, economic and technological demarcation lines. No longer is enterprise connectivity considered blasé, implemented by rote where purchase decisions are predicated solely on cost. Nor is it one-size-fits-all but comes in all shapes and sizes. Enterprises are realizing that IoT connectivity planning, development (or selection) and implementation require careful consideration of a broader set of criteria, purpose-built to deliver downstream ROI in both economic and socio-environmentally sustainable terms.

Get Connected in One Click

Request Your IoT Connectivity Starter Kit

Endnotes

- Tobias Ryberg, The Global M2M/IoT Communications Market Third Edition IoT Research Series, 2018, (Gothenburg Sweden, Berg Insight Research Team, 2018), 1.

- Knud Lasse Lueth, State of the IoT 2018: Number of IoT devices now at 7B – Market accelerating, (IoT Analytics GmbH, Hamburg, Germany, 2018), https://iot-analytics.com/state-of-the-iot-update-q1-q2-2018-number-of-iot-devices-now-7b/.

- Ryberg, The Global M2M/IoT, 144.

- Ibid., 141.

- Ibid., 2.

- Ericsson, IoT connections outlook, (Telefonaktiebolaget LM Ericsson, Stockholm, Sweden, 2018), https://www.ericsson.com/en/mobility-report/reports/november-2018/iot-connections-outlook.

- GSMA, Mobile IoT in the 5G Future, (GSM Association, London, UK, 2018), 2.

- Ryberg, The Global M2M/IoT, 7.

- Ibid.

- John Walko, 2G Sunset a Slow Burn, (AspenCore, Inc., Cambridge, MA, 2017), https://www.eetimes.com/author.asp?section_id=36&doc_id=1331112.

- Verizon, CDMA Network Retirement, (Verizon, New York, n/a), https://www.verizonwireless.com/support/knowledge-base-218813/.

- Natalia Szczepanek, Satellite IoT Forecast 2019–2024, (Rethink Research, Bristol, UK, 2019), https://rethinkresearch.biz/report/satellite-iot-forecast-2019-2024.

- Ibid.

- Ibid.

- GSMA, Narrowband – Internet of Things (NB-IoT), (GSM Association, London, UK, 2018), https://www.gsma.com/iot/narrow-band-internet-of-things-nb-iot/.

- Jorge Sa Silva; Pei Zhang; Trevor Pering; Fernando Boavida; Takahiro Hara; Nicolas C. Liebau, People-Centric Internet of Things, (IEEE Communications Magazine, New York, 2017), https://ieeexplore.ieee.org/document/7841465.

- Ryberg, The Global M2M/IoT, 87.

- Carrie MacGillivray, Stacy Crook, IDC’s Global IoT Decision Maker Survey, 2019 First Look, (IDC Framingham, MA, 2019), 6, 12, 14.

- Ibid., 7, 16.

- Ibid., 9, 11.

- Ibid., 10, 15.

- Ibid., 8.